With more than 2.3 million Vietnamese immigrants living across all 50 U.S. states, the Vietnamese-American community reflects every level of economic reality. Some have built successful businesses and achieved great wealth. Others still rely on public assistance, food benefits, or struggle with housing insecurity.

Yet despite those differences, many share one common priority: trying to save a little money to send back home and help family members in Vietnam.

Whether it is a modest monthly transfer or occasional support during difficult times, these remittances represent more than money—they are acts of responsibility, love, and connection to one’s roots. Individually, the amounts may seem small. Collectively, they add up to enormous sums.

![]()

Vietnam’s Growing Remittance Flow

According to reports from Vietnam, Ho Chi Minh City alone received a record $10.34 billion in remittances in 2025, an increase of 8.3% compared with 2024.

Roughly 60% of all overseas remittances sent to Vietnam are concentrated in Ho Chi Minh City, while the remaining 40% is distributed across other provinces and cities.

It is important to note that these official figures only reflect money sent through licensed and documented transfer channels. They do not include cash carried by travelers, informal hand-delivery networks, or undocumented transfers. In reality, the total amount reaching Vietnam is likely much higher.

The Global Remittance Iceberg

The Remittance Iceberg

Statistics from multiple sources estimate that between $80 billion and more than $200 billion leaves the United States each year through money transfers. Because these funds move through many different channels—both official and unofficial—the numbers vary, and no one can collect complete data precise enough to determine an exact total.

The leading remittance-sending communities are:

- People of Mexican origin: $62.5 billion

- People of Indian origin: $38 billion

- People from Guatemala: $20 billion

- Filipino community: $16 billion

- People of Chinese origin: $12.7 billion

The United States is a nation of many ethnic communities, and nearly every group sends something back to loved ones in their homeland—whether large or small. Even care packages filled with Green Oil (Dầu Gió Xanh), Tylenol, Glucosamine, and other household goods represent money sent home in another form.

Still, the figures above are only estimates and do not fully reflect reality.

Sending money has long been simple and convenient. A sender only needs to provide the names and addresses of both sender and recipient, along with the amount, and complete the transaction at a transfer counter.

In less than 24 hours, family members often receive the full amount in U.S. dollars or local currency, without losing a cent to taxes from either side. Transfer fees are usually paid in the United States.

The issue now is that hundreds of billions of dollars have continued flowing out of America year after year—rising and falling at times, but never stopping. That steady outflow has become a growing concern for the IRS and the U.S. Department of the Treasury.

And that concern is now being converted into revenue: taxation.

Projected collections are estimated to reach $10 billion over the next 10 years.

What Payment Methods May Avoid the Tax?

According to the IRS, there are currently about 600 licensed money transfer businesses operating in the United States. Of those, more than 200 companies operate through networks totaling roughly half a million agents.

Between 2019 and 2024, the total amount of money transferred to domestic and international destinations through money transfer services increased from $1.3 trillion to $4 trillion.

Remittances—money sent abroad—accounted for 9% to 25% of all transferred funds. Specifically:

- $236 billion in 2019

- Nearly $1 trillion in 2021 and 2022

- An estimated $365 billion in 2024

According to the World Bank, total global remittances reached $905 billion in 2024, with money sent from the United States ranking first and accounting for roughly one-third of the total. That is one reason why the dream of earning money in America continues to attract immigrants from around the world.

With a 1% tax imposed on senders, the U.S. Treasury collects new revenue, while senders must pay more to support their families abroad. For example, if people of Mexican origin send $62.5 billion to relatives in Mexico, they would need to pay an additional 1% in order for the full $62.5 billion to arrive.

On the other hand, some families may reduce the amount they send in order to offset the tax, meaning recipients receive less. Simply put: the more you send, the more tax pressure you face.

Countries receiving large volumes of remittances—including Vietnam, China, India, Guatemala, and El Salvador—could feel the effects. In time, some recipient governments may even consider taxing incoming remittances themselves if declining inflows begin to affect public finances.

From the perspective of the current administration, the estimated $365 billion sent out of the United States each year does little to stimulate the domestic economy beyond supporting transfer businesses. That money is not being spent in U.S. stores, restaurants, or local services, which means no indirect consumption tax revenue is generated domestically.

This new 1% excise tax on remittances, established under the One, Big, Beautiful Bill, was approved by the U.S. Congress.

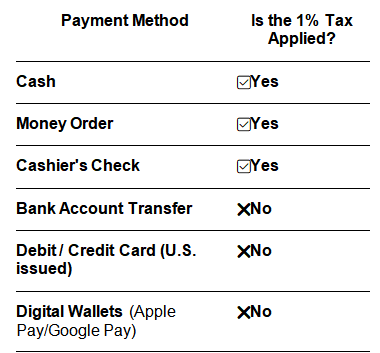

According to the chart above:

Subject to the 1% Tax

- Cash

- Money Orders

- Cashier’s Checks

Exempt from the 1% Tax

- Bank Account Transfers

- Credit Cards

- Debit Cards

- Digital Wallets (Apple Pay, Google Pay, etc.)

-Đức Hà-

Special to HuuTri.org